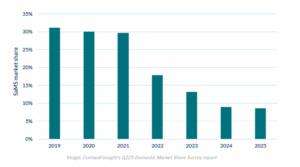

Cornwall Insight’s latest Domestic Market Share Survey says this marks a drop from 8.9% in the previous quarter and a dramatic fall from the 31% share held before the energy crisis began.

The country’s six largest energy providers – British Gas, E.ON Next, EDF, Octopus Energy, OVO and Scottish Power – now control 91.3% of the domestic energy market.

This growing dominance reflects continued market consolidation and the effects of the energy crisis, which saw 26 suppliers, nearly all in the small and medium category, exit the market.

The latest decline was partly driven by British Gas absorbing 84,000 customers from Rebel Energy under the Supplier of Last Resort (SoLR) process, alongside updated customer data for other smaller suppliers.

Many SaMS were unable to weather the severe wholesale price volatility during the crisis, unlike their larger counterparts with more substantial capital reserves.

Although market conditions have improved since the peak of the crisis, smaller suppliers still face tight margins. High wholesale costs remain a challenge and new regulatory responsibilities from Ofgem are adding further strain, especially for firms without dedicated compliance teams.

New supplier entries into the market have also slowed. Since 2021, only three suppliers have joined the domestic market, compared to 17 new entrants in 2017.

Matthew Smith, Analyst at Cornwall Insight, said: “We’re continuing to see the effects of the energy crisis play out in the domestic market. The numbers show a continued shift away from a highly competitive, fragmented supplier base towards a more consolidated market dominated by the biggest players.”